NAIROBI: UNRAVELLING the true story of why certain things are the way they are requires critical thinking and rigorous analysis.

In this case, to fully understand the problems Kenya faces, particularly in repaying its debts, and to unravel the corruption and inefficiencies that are preventing the government from delivering to its people, it is important to examine and analyse information from Kenyan sources and reputable international agencies to assess the state of Kenya’s economy.

For example, financing the construction of the SGR from Mombasa and connecting it to Nairobi-Naivasha with a large $5.3 billion loan, over and above the market rate, much as many wouldn’t like to hear it, is forcing the government to draw on dwindling reserves and resort to expensive Eurobond refinancing to manage debt payments.

Loan providers are no longer the only ones concerned about this situation; Kenyans, particularly Generation Z, view the actions being taken as a struggle for their future.

In practice, this suggests that Kenya still has a significant amount of work to do to fortify its economy and ensure that Kenyans can reap the rewards of their nation.

As an economics analyst specialising in EAC economic and investment performance, utilising and analysing each nation’s central bank data, CAG reports, and National Bureau of Statistics data, one can readily comprehend the challenges facing a given nation’s economic growth, as such scrutiny allows one to identify the underlying issues, given that facts and data don’t lie.

It is widely noted that Kenya has long been portrayed as having the largest economy in the region, but a thorough analysis of authoritative sources produced by Kenyan scholars and researchers, as well as by global institutions such as the World Bank and the IMF, reveals discrepancies in this portrayal, suggesting the economic problem Kenya is facing today has a genesis worth unpacking. History is consistently recommended as an exceptional subject in education.

Additionally, it is recommended that history provides the opportunity to identify one’s shortcomings and determine how to proceed. In this instance, I would like to rewind a bit to provide a clearer understanding of the underlying causes of Kenya’s economic woes.

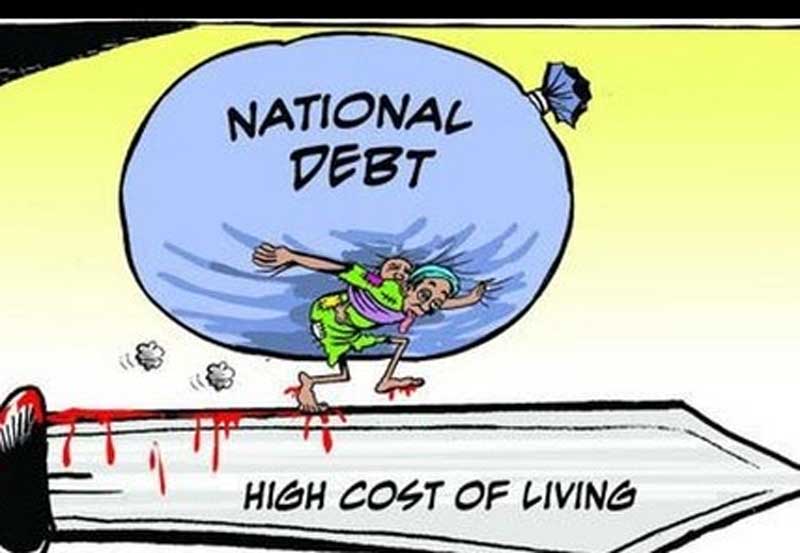

This factor is contributing to Kenya’s continued economic decline as it transitions from the robust, dependable economy that the world has come to expect. Kenya’s debt has grown substantially over the past 15 years.

In 2010, government debt stood at a manageable 39 per cent of GDP; by March 2023, it had risen to 68 per cent of GDP. Depending on the calculation methodology and exchange rate effects, Kenya’s public debt remained at 68 per cent of GDP in 2024. According to World Bank reporting, debt stood at 68.8 per cent of GDP in 2025.

This increase in debt, when viewed through an economic lens, is the consequence of a significant rise in borrowing from 2013 to 2022, during which substantial loans were extended to finance infrastructure initiatives following robust expansion in the early 2000s.

What is striking from Kenyans’ own sources is that many of these initiatives failed to generate sufficient economic expansion to justify their expenditures.

For instance, the $5.3 billion loan to finance the Standard Gauge Railway (SGR) project, which links the coastal city of Mombasa with the capital, Nairobi, is often cited as an example of excessive borrowing.

ALSO READ: Govt: National debt sustainable

Corruption, which diverted funds from substantial loans, affected numerous infrastructure projects. In particular, the Kenyan government’s allocation of substantial international loans has been the subject of substantial allegations of misappropriation.

According to estimates by the consulting firm Odipo Dev (for details, see the elephant.info), which analysed the visual history of Kenya’s corruption scandal, the government incurred losses of at least 567.4 billion Kenyan shillings ($4.4 billion) due to corruption between 2013 and 2018.

Transparency International’s Corruption Perceptions Index has consistently ranked Kenya 139th out of 180 countries, with a score of 27, over the past ten years.

The Kenyan shilling has also declined by 31 per cent against the US dollar during this period.

Although this can be viewed as advantageous for Kenyan exporters, particularly those exporting tea, cut flowers, tropical fruits, and coffee to Uganda, the USA, the UAE, the Netherlands, and Pakistan, which accounts for 9.8 per cent of their exports, Kenya’s debt repayment is significant and will remain influenced by the dollars it generates from exports, particularly given that the nation imports more than it exports.

According to 2022 data, Kenya’s trade deficit was approximately $18 billion. Kenya imports petroleum, palm oil, wheat, packaged medicines, and rice, with the principal sources being China, India, the UAE, the USA, Malaysia and Tanzania.

Scanning through what is being exported versus imported and the commitment to repay the loans, the treasury is confronted with a substantial challenge as a result of the shilling’s decline in value.

The majority of Kenya’s $80 billion debt is denominated in dollars, and the depreciation of the shilling has substantially burdened these repayments. Kenya, a nation in debt distress, frequently encounters unscrupulous creditors and lenders.

Debt Justice, a campaign group that commented on Kenya’s economic crisis (see the African Forum on Debt and Development (AFRODAD) in 2024), has stated that Kenya’s debt is the root cause of the crisis.

This debt is the result of irresponsible lending by development partners, including the World Bank and the International Monetary Fund, and of Kenya’s insatiable appetite for borrowing, which has led to the issuance of bonds with double-digit interest rates.

In my view, Kenya needs responsible borrowing and the effective use of loans to contribute to Kenya’s development agenda.

As it stands, new loans are now being used only to pay old debts, leaving Kenyan citizens further indebted.

Without going into the details of how inflated SGR costs, massive project overvaluation, revenue underperformance, toxic cargo guarantee clauses, reduced budget flexibility, forced currency conversion, debt maturity extension, and competition with Eurobond refinancing and debt maturity extension, the government has had to extend the loan tenure (now until 2040) and utilise grace periods to avoid immediate default, which, in my view, only pushes the massive liability further into the future.

Overwhelmed by the brief trend highlighted earlier, events in June 2024 led Kenya into a deeper economic crisis, with a June 2024 deadline to repay a $2 billion Eurobond issued in 2014.

In January 2024, the International Monetary Fund (IMF) provided a $941 million loan, increasing the organisation’s total exposure to Kenya to $4.4 billion.

It was reported that Kenya secured $941 million in IMF loans to ease financing pressures. Kenya issued a $1.5 billion international bond at a 10.4 per cent interest rate to address the remaining deficit.

While considering international markets, it might appear like they are welcoming the second loan, as they no longer anticipate an imminent Kenyan debt default; as economists and investment experts see it, Kenya’s double-digit debt costs are a sign of tough times ahead.

The key question is whether Kenya realised what lay ahead. In fact, this level of interest payment for Kenya is a stark warning of financial ill health.

It is worth noting from an experience of analysing nations’ economies that six of the fifteen nations that have issued bonds at interest rates of 9.5 per cent or higher since 2008 have ultimately defaulted.

In Kenya, the decision to pay over 10 per cent on a new international bond to prevent a default later in the year, despite a history of such gambits resulting in financial losses, underscores the extent of Kenya’s economic distress.

Although interest rates have increased globally in recent years, a double-digit financing cost remains one of the most evident indicators that a nation is not in good economic health.

Many Kenyans recall that Ruto’s government agreed to tax increases in exchange for a low-interest IMF loan.

This was followed by the introduction of a finance bill outlining the government’s intention to raise 346 billion Kenyan shillings ($2.68 billion).

These proposals triggered mass protests among Gen Z, who at every level saw their future put at the crossroads.

The protests were followed by violence, resulting in the deaths of demonstrators and drawing global attention to Kenya’s political and economic challenges.

Undeniably, the Kenyan economy is in a difficult situation, particularly during this period as it prepares for the 2027 general elections, given these factors.

The question is, where will Kenya conceal its arrogant visage as the largest economy in the East African region?